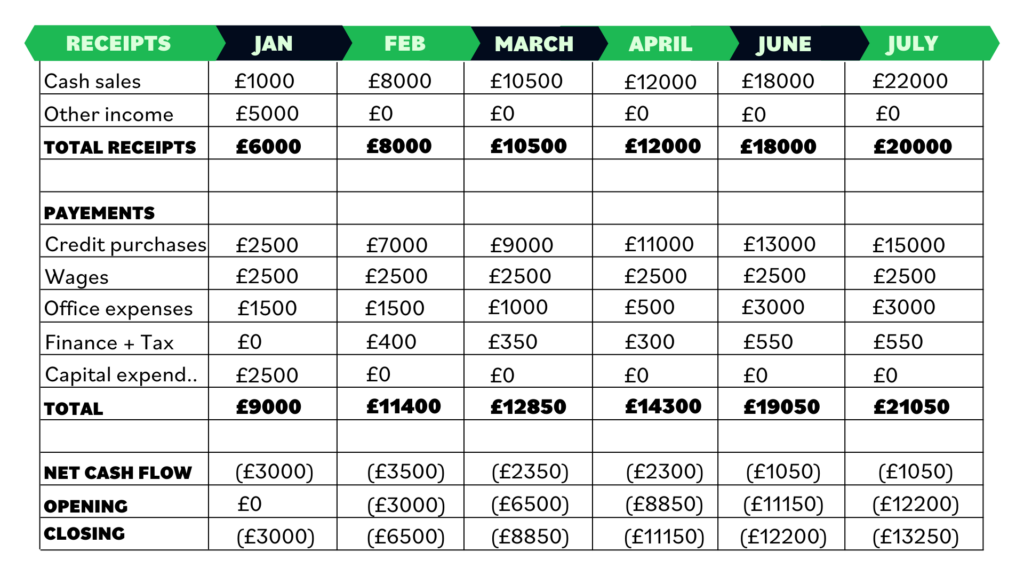

A cash flow forecast is a prediction of how much money is coming in and out of the business over a certain period of time. As well, forecasting cash flow is a beneficial tool that helps business planning- already off to a good start if it helps planning!

For businesses forecasting cash flow can be time-consuming but does introduce key accounting concepts such as fixed, variable and capital costs; all in which described below . A lot to think about but all very much important to your business.

What is cash flow forecasting?

Let’s start with that a cash flow forecast is a method that shows how and when a business expects to receive and make ‘cash’ payments over a certain period of time. Most time periods are 6-12 months.

This method is key to either a start-up or running a business as it works as a decision-making tool as well as helping to identify:

For a start-up: how much initial investment is needed to start?

Whereas for a running business: what cash flow problems might occur along the way? Taking on new staff, if the business grows substantially.

Aspects to consider for a cash flow forecast

After discussing what cash flow forecasting is. The preparation for a cash flow forecast involves more than just itself. There are factors such as a sales forecast and key business concepts to consider.

Simply, a sales forecast is estimating future sales and the revenue it will generate over a certain period of time. As you can see it closely relates to a cash flow forecast. The difference is that a sales forecast focuses on the sales of products and services instead of just the whole businesses cash sales.

To learn more about sales forecasting take a look at Sales Forecasting: Making It Make Sense.

Next is the different types of business costs that a business should understand when preparing, these are;