Let’s begin with a general overview of what a profit and loss account is.

A profit and loss account is a record that provides information on how a business has performed over a specified period of time including a summary of total income and expenses. For formal accounts this is usually 12 months, for a management account it’s one month.

Commonly, a P&L account can be known as an ‘income statement’.

Profit will be shown if income is greater than expenses and loss will be shown if expenses are greater than income.

All limited companies are obligated to prepare an annual profit and loss account to comply with company law. However, sole traders, self-employed individuals and partners in regular business partnerships, don’t have any legal obligation to present an annual profit and loss account.

Even though it is not a legal obligation. The P&L accounts are a key part of the annual financial statements of a business. It pairs nicely with the balance sheet statement. To learn more about Balance Sheets visit the link here: https://enterprisemadesimple.co.uk/guide-to-balance-sheets/

Understand Your Profit

Profit is a simple but important concept. To calculate profit, all a business needs to do is work out the difference between the income and its expenses. A loss will occur if expenses are higher than income.

If profit within a business isn’t consistent, money will be exhausted and the business will fail. In difference, if a business can successfully generate a consistent stream of income, it will be able to grow and surplus profits may be shared within owners.

What’s included in a P&L account?

In a profit and loss statement a business owner is able to see:

- The income from a specific period of time.

- Business expenses from the period chosen. Any costs associated with sales and all other business expenses are included.

- The profit or loss attained in this period.

A profit or loss account is usually prepared for the 12-month period that is in correspondence to a business’s financial year.

To prepare a profit and loss account monthly is good practice as a part of the regular management of accounts within a business.

Key terminology

Sales turnover

A sales turnover is the invoice of the sales of products and services during the period shown in the profit and loss account, this excludes VAT the business is VAT-registered. FYI, it does not represent the actual amount of money retrieved from customers as some payments can be outstanding or have been paid in advance.

Cost of sales

Cost of sales, can be known as direct or variable costs, are the costs that could be directly attributed to the production of a product or sale of an item.

For instance, if a company made special occasion cards, the cost of sales would be the cost of the raw materials like paper, glue, ink etc; this is the total cost of how much it is to create each product.

A small company wouldn’t have the same cost of sales as a large company, not due to the increased sales but because a large company can put the cost of labour used for production as direct costs. Whereas a small business generally doesn’t hire and fire to keep up with the pace of demand.

For retail businesses, the cost of sales is seen as the cost of stock items being sold.

A service business would not usually show a figure for cost of sales.

Remember, the cost of sales should equate to the cost of producing the goods that have actually been sold and doesn’t necessarily account for all the payments for raw materials that the business has made in the period covered in the P&L account.

Unused raw materials and unsold products are shown on a balance sheet as stock. To learn further about balance sheets read more here: https://enterprisemadesimple.co.uk/guide-to-balance-sheets/

Gross profit

Gross profit also known as ‘contribution’, is the difference between sales turnover and the cost of sales.

Why is it known as ‘contribution’? This is because it contributes to the overhead costs of the business and, when these are paid for, it contributes towards net profit.

Administrative expenses

This includes rent, utilities and all operating expenses that are not directly related to producing the product.

These costs can be known as ‘overheads’, but generally they’re related to fixed costs as they don’t rise or fall in direct proportion to output.

Operating profit

Operating profit is referred to as ‘profit before interest and tax’. This just means its the profit generated after all usual administrative expenses have been deducted.

Tax on profit

Corporation tax is chargeable on the profits of a company and any amount shown in the distribution account below the P&L account.

The actual calculation of the tax due will be adjusted to take account of those expenses not allowed for tax purposes (generally depreciation) and to include those items that are allowed for tax purposes (such as capital allowances).

A sole trader or partner will pay income tax on the trading profits so a tax charge is not shown in their P&L account. The tax charge is calculated through their self-assessment tax return instead.

Net profit

Net profit, which can be known as ‘profit after tax’, is usually distributed between owners of the business or held and used to fund growth.

Putting the profit and loss account to work

For a business owner to monitor their business performance it is important that when reviewing their profit and loss account, to review the balance sheet and the cash book alongside.

This then helps to generate a good overview of the business performance.

It is useful to regularly review the business performance monthly if you can do so, however, to review yearly is still important. Reviewing these documents helps to see actual figures of what the business set to achieve versus what they did achieve.

By reviewing areas such as goals originally set versus the outcome allows a business owner to identify whether the business achieved these goals or not. Further, if the business has not succeeded, by reviewing it grants a business to re-evaluate and work out how to achieve these goals in the next year.

Further, if a business has been running for a while, it is useful to compare the performance of the business from this year against the previous year proving a useful benchmark of progression in the business over the year.

Don’t forget! It’s important to factor in any relevant industry or market trends to get the biggest picture.

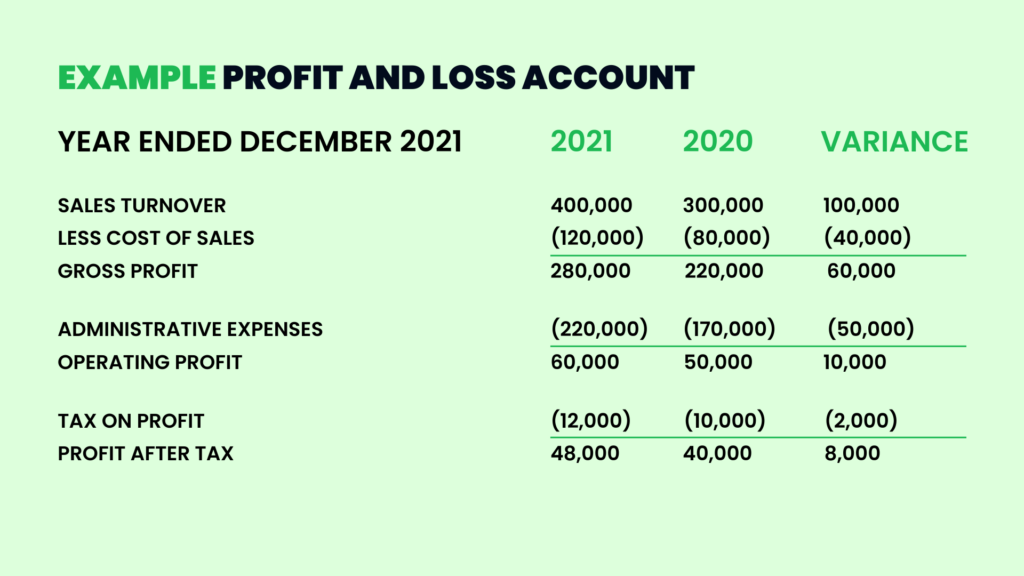

Example of a P&L account

For instance, turnover is up, as are all of the profit indicators such as gross, operating and after tax. With the turnover increasing by 33% is still great, however, the profit has only increased by 20%. This is a good starting point to investigate why this is.

The following table shows a deeper look into this.

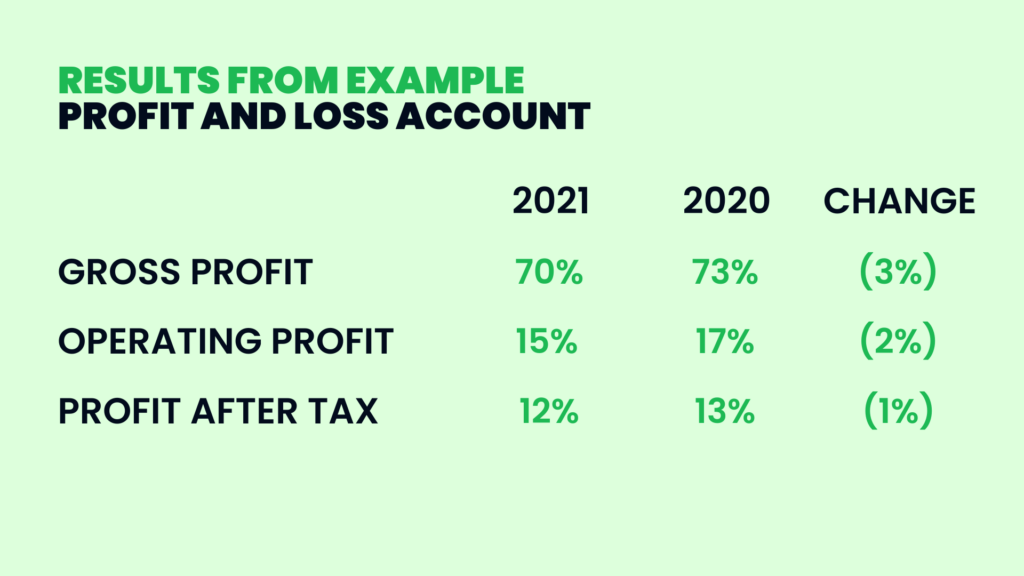

Taking a look at the percentages shows that the relative profit has dropped against the other profit indicators.

A profit after tax in the year 2020 of 13% would have accumulated £52,000 rather than the £48,000 actually achieved.

That is just an example of what a business should be looking for when evaluating the Profit and Loss account.

Further research should be asking these questions:

- Are selling prices under pressure from other competitors?

- Has raw materials increased faster than selling prices?

- What is the reason for overhead costs increasing so quickly?

Taking into consideration all of these questions will help to gather critical information on where there is a need to bring in a strategy that will improve profitability.

Going into more detail

If a company was to do regular monthly management of the account, then more detail is required than the typical format of an annual report above.

The typical format above is still advised to be used. More detail just means that areas should be more sectioned to the details of the business. As for example, the sales turnover can be sectioned into showing income for each of the main product lines, so on, for the cost of sales. Administrative expenses can be split into things such as staff, premises and marketing etc.

Accrual Accounting

One basic principle of accounting is to match income and expense to the period that is being recorded which is known as Accrual Accounting. This provides the most accurate assessment of net profit for the period.

Some companies tend to record income and expenses in their Profit and Loss accounts on the basis of the date of the sale or purchase invoice, instead of the day cash is received. In most cases, this is satisfactory, but, in some other cases it isn’t. Especially, near the end of the year. Recording income and expenses this way can lead to an over-or understatement of profit.

It is important for business owners to discuss with their accountant whether accrual accounting will impact their business. Accrual accounting may need to be taken into account when preparing a regular management account.

In contrast to regular managerial accounting, if the income and expenses are quite straightforward then only minor adjustments will be required at the year-end.

Heads up! If annual accounts are prepared using accrual accounting, then so should profit and loss accounts.

Profit and Loss accounts only do so much…

A profit and loss account is still vital to a business but it does need other documents beside it to provide the full picture.

This specific account shows the profit of said business, but does not show the cash position of the business. A cash flow forecast is what would help to acquire the cash position. To learn more about Cash Flow Forecasting Click Here!

Further a profit and loss account doesn’t show the solvency of a business. But what does is a balance sheet! To have a strong balance sheet helps a business to survive long period of losses, whilst a weak balance sheet will cause a business to fail much quicker once trading losses begin.

To learn more about how to create your own strong balance sheet read: https://enterprisemadesimple.co.uk/guide-to-balance-sheets/

Reach out!

If you need further guidance on the financial side of the business come to us! EMS has business advisors dedicated to guiding you through these subjects. Contact us here.